Paying for Solar in NZ: Cash vs Green Loans vs Personal Loans (2026)

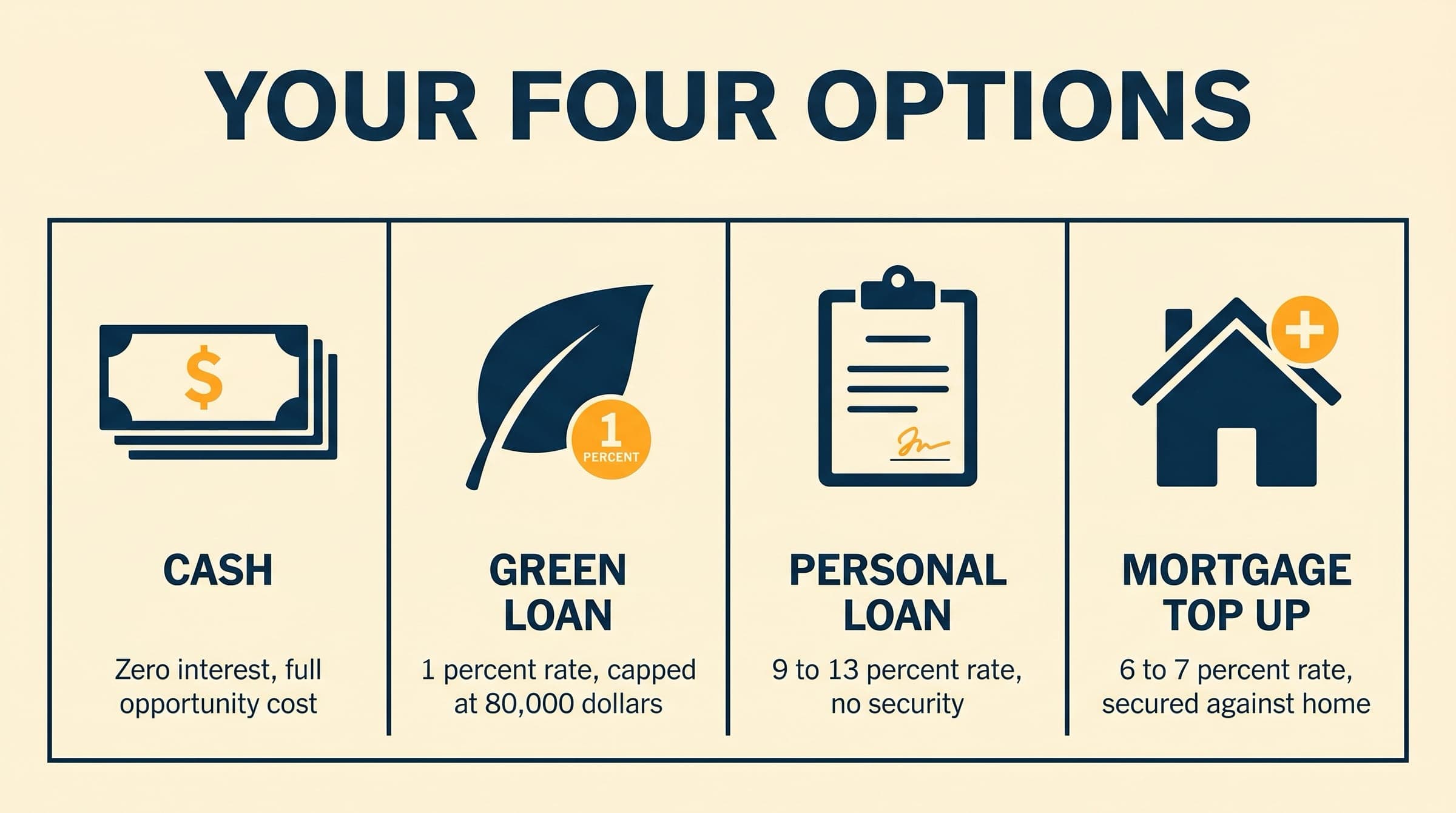

Your Four Options

There are four ways to pay for a solar system in New Zealand. Each comes with different trade-offs around upfront cost, total cost, and flexibility. For a deeper look at NZ-specific subsidies and bank green loan terms, see our guide to solar grants and incentives in NZ.

- Cash upfront ($15,000 to $25,000 out of pocket). No interest, no monthly payments, instant ownership. The simplest option, but it ties up a significant chunk of capital.

- Green home loan (0 to 1% from major banks). Requires an existing mortgage and at least 20% equity. This is the cheapest way to borrow. Most NZ banks now offer green loan products specifically for solar.

- Personal loan (7.99 to 16%+ from banks or Harmoney). No mortgage needed. Available to renters and mortgage-free homeowners, but significantly more expensive over the life of the loan.

- Do nothing and keep paying rising power bills. Electricity prices in NZ have risen 5 to 7% per year for the last decade. Doing nothing is not free. It just means the cost is spread across your monthly power bills instead of a solar system.

Over $1 billion in green loans have been issued in NZ since 2023. The banks want to lend for solar. The question is not whether you can get financing. It is which option costs you the least over time.

The cheapest way to pay for solar is not always the obvious one.

The Real Maths: $15,000 System

This is the money shot. A standard 6.6 kW solar system costs around $15,000 installed. Here is what you will actually pay depending on how you fund it. The full installed-cost breakdown by system size is in our NZ solar pricing guide if you want to sanity-check the $15,000 figure for your roof.

The difference between Westpac 0% and a 13% personal loan on the same system is $5,519. That is a second set of panels you could have bought instead.

Already know you want solar? Get quotes from vetted installers and we will help you find the right financing.

The Real Maths: $25,000 System with Battery

Adding a battery pushes the total system cost to around $25,000. The financing gap widens even further at this price point.

On a $25,000 system, the wrong financing choice costs you up to $9,199 in unnecessary interest. That is nearly 37% more than the system price.

power bill?

Why Cash Isn't Always King

Conventional wisdom says paying cash avoids interest. That is true. But it ignores what else your money could be doing. Whether financing solar is a good move ties back to whether it pays back at all: see our full payback breakdown for NZ households.

The opportunity cost

If you have $15,000 sitting in savings, here is what it could earn you over 5 and 10 years compared to putting it all into solar upfront.

Solar savings are tax-free. Investment returns are not. A $2,000/year solar saving is equivalent to earning about $2,780 pre-tax in an investment account.

Property value uplift

- NZ data shows homes with solar sell for 3 to 4.4% more than comparable homes without it.

- On a $700,000 home, that is a $21,000 to $35,000 premium.

- The system pays for itself AND adds equity to your property.

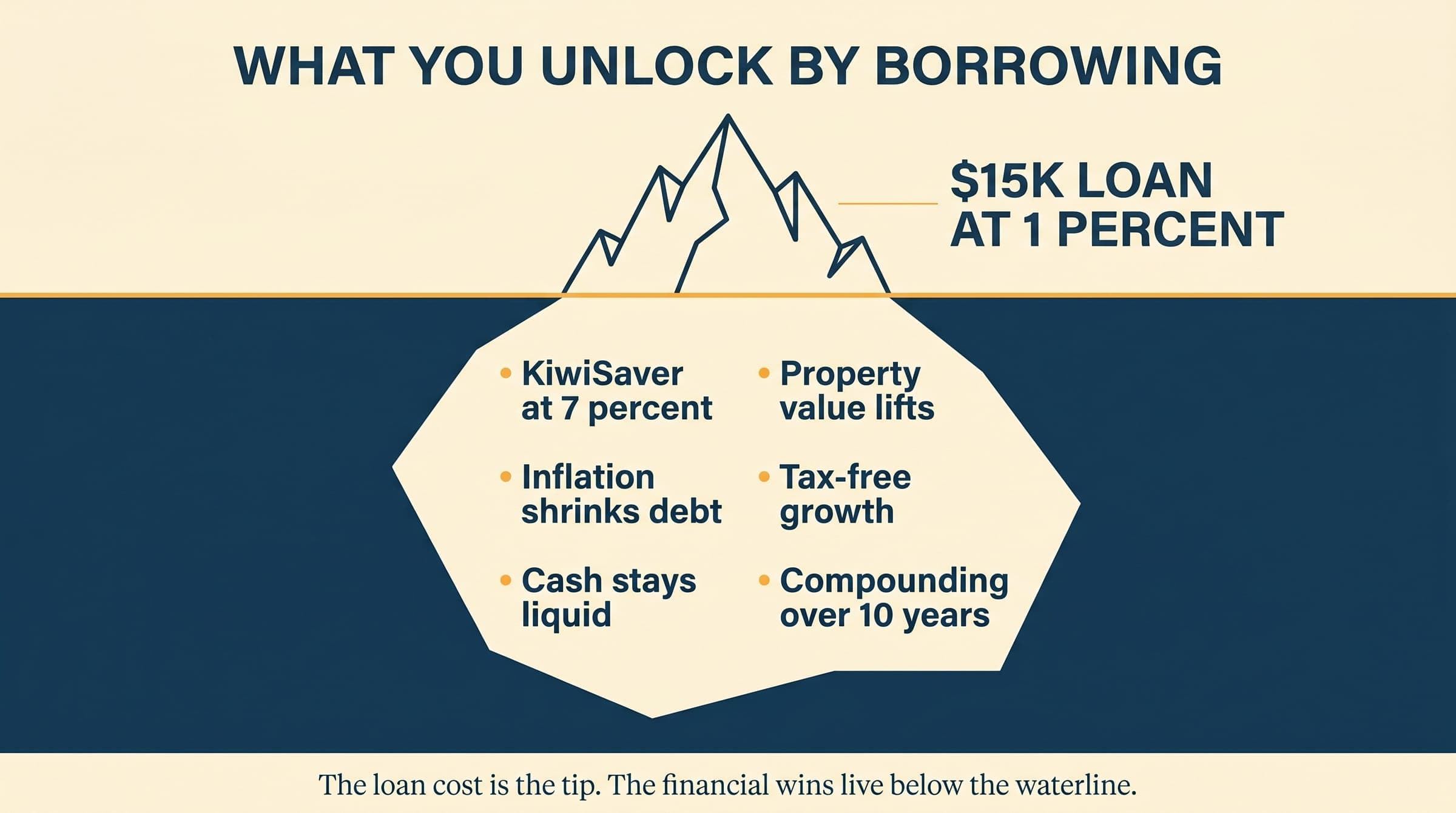

The "Best of Both Worlds" Play

This is the insider move. Borrow at 0% from Westpac. Keep your $15,000 in a term deposit earning 3.70%. Over 3 years you earn ~$1,238 after tax in interest, while paying exactly $0 in loan interest. Meanwhile your solar system saves you ~$2,000/year in power bills.

Borrow at zero, earn at 3.7%, save $2,000 a year on power. That is not a loan. That is an arbitrage.

Even with ANZ/ASB at 1%, the arbitrage works. You pay $232 in interest but earn ~$1,238 from your term deposit. Net gain: ~$1,006.

Six Gotchas Nobody Mentions

1. The post-term rate trap

- ANZ/ASB revert to ~5.79% floating after the 3-year fixed period ends.

- BNZ reverts to ~8.69% floating. Significantly worse.

- Westpac reverts to 5%. Still the best of the lot.

- If you have not paid off the loan within the fixed period, your monthly payment jumps dramatically.

Pro tip: Set up automatic payments calculated to clear the full balance within the fixed period. Do not rely on minimum payments.

2. Quote expiry catches you out

Get your loan pre-approved first, then get the installer quote. Not the other way around.

3. Break fees if you sell or refinance

- 1% fixed loans have break fees. They are small but real.

- Westpac 0% has NO break fees. Another reason it is the best option.

- If you move banks to get a better mortgage deal, break fees apply to the green loan portion.

4. Your installer goes bust

- Product warranty (from the manufacturer) survives. Workmanship warranty does not.

- The Consumer Guarantees Act lets you claim against the manufacturer or importer directly.

- SEANZ membership provides some protection.

- This is why choosing a vetted, established installer matters more than saving $500 on a quote.

5. Insurance: you must notify your insurer

- Roof-mounted panels are covered under your existing home insurance policy.

- You MUST update your sum insured to include the system value.

- Failure to notify your insurer means the panels may not be covered if something goes wrong.

- Premium increase is modest, roughly $20 to $30 per year.

6. Meter upgrade is not always free

- An import/export meter costs approximately $150 to $195.

- Some retailers cover it. Others pass the cost to you.

- It takes 3 to 5 weeks to arrange.

- This cost is not included in most installer quotes, so budget for it separately.

When Financing Doesn't Make Sense

Solar financing is not always the right call. Here are the situations where paying cash or waiting makes more sense.

Small systems under $8,000

Monthly savings from a small system are too low (roughly $800 to $1,200 per year) to justify the complexity of a loan. If you can afford to pay cash for a system this size, do it.

Selling within 2 to 3 years

Solar payback is 5 to 8 years. If you sell before breakeven, you are unlikely to recoup the full cost through the sale price premium. Break fees add cost at sale too.

Exception: Westpac 0% with no break fees, combined with the property value uplift, can still work if you are selling in the medium term.

Power bill already under $150/month

With savings of only $1,000 to $1,200 per year, the payback period stretches to 10+ years. Financing costs erode those thin savings further. Solar may still be worth it for environmental reasons, but the financial case is weaker.

No mortgage

You cannot access green loans. They are all structured as mortgage top-ups. Personal loans at 8 to 13% make solar significantly more expensive. Some banks may open a small mortgage specifically for the purpose, but this adds complexity and fees.

Already stretched on debt

CCCFA affordability rules may mean you are declined anyway. Adding debt when you are already tight is risky regardless of the long-term savings. Solar saves money over years, but it will not fix short-term cash flow problems.

Your Rights as a Borrower

Cooling-off periods

- 5 working days if you signed in person.

- 7 working days if the contract was sent by email.

- 9 working days if the contract was sent by post.

You can cancel the credit contract in writing during this period. Note that buy-now-pay-later purchases do not have a cooling-off period.

CCCFA protections

- Banks must assess affordability. They cannot lend if repayments would cause substantial hardship.

- All terms, rates, and fees must be clearly disclosed before you sign.

- Green loans must state what rate applies after the promotional period ends.

Consumer Guarantees Act

- Solar installation is both goods and services. Both are covered.

- The system must be of acceptable quality and fit for purpose.

- These rights cannot be contracted out of.

- Resolution path: installer first, then manufacturer, then the Disputes Tribunal.

Common Questions

What's the cheapest way to pay for solar in NZ?

Westpac’s 0% Greater Choices loan for 5 years. You pay exactly the system price with zero interest and no fees. If you are not a Westpac customer, ANZ and ASB at 1% for 3 years cost just $232 in interest on a $15,000 system.

Can I get a green loan without a mortgage?

No. All NZ bank green loans are mortgage top-ups requiring an existing home loan. Without a mortgage, your options are cash, personal loan (7.99%+), or establishing a small mortgage specifically for the purpose, which adds complexity.

What happens to my green loan if I sell the house?

The loan is repaid from sale proceeds like any mortgage. If you are on a fixed 1% rate and sell mid-term, you may face break fees. Westpac’s 0% loan has no break fees, making it the best option if you might sell.

Should I pay cash or take the 0% loan?

Take the loan. Put your cash in a term deposit earning 3.70%. You earn ~$1,238 in interest over 3 years while paying $0 in loan interest, AND you get $6,000+ in solar savings. There is no mathematical reason to pay cash when 0% financing exists.

What if my bank doesn't offer a green loan?

Switch banks, or check if your bank has recently launched one. Most major NZ banks now offer green loan products. Alternatively, take the best personal loan rate you can find and plan to pay it off as fast as possible to minimise interest.

Will solar panel prices drop if I wait?

No. Prices rose 9% in Q4 2025 and are forecast to increase another 10 to 30% in 2026 as China tightens production. Every month you wait, you are paying full retail power prices AND facing potentially higher panel costs. The best time to buy was last year. The second best time is now.

Next steps for your solar journey

Written by Harnill Hylan

Harnill is a software developer specialising in computer vision and aerial imagery. He designs the analysis engine behind every Solar Scout report, turning satellite images and roof data into the actual numbers Kiwi homeowners can trust. He writes Solar Scout's guides on system performance, monitoring, and the data side of solar.

Related guides

View all

Solar Finance NZ: Green Loans Compared (2026)

Compare NZ solar green loans: Westpac 0%, ANZ 1%, ASB 1%, BNZ 1%, Kiwibank variable + cashback. Eligibility, terms, and which is best for you.

Can I Claim Solar Panels on Tax in NZ? (2026)

How solar interacts with NZ tax, by audience. Owner-occupier, landlord, business, lifestyle block, Air BnB, and buy-back income. General info, not tax advice.

Solar Panel Grants and Incentives NZ (2026)

What financial help is available for solar in NZ? Green loans, EECA programmes, and what NZ doesn't have compared to Australia and the UK.

Solar Panel Costs NZ: What You'll Actually Pay in 2026

Real pricing data for NZ solar in 2026. System costs by size, what affects price, and how to tell if a quote is fair.